Projects

Impact

About Klub

Klub Capital India is a revenue based financing platform, that helps digital businesses and SMEs grow by offering flexible funding.

Klub partners with NBFCs, HNIs & financial institutions to provide capital.

Whether a business is in its early, growth, or late stages, Klub offers tailored funding solutions for recurring expenses like marketing, inventory, and capex, helping businesses thrive at every stage.

650+ brands have raised funding with Klub.

How it all began?

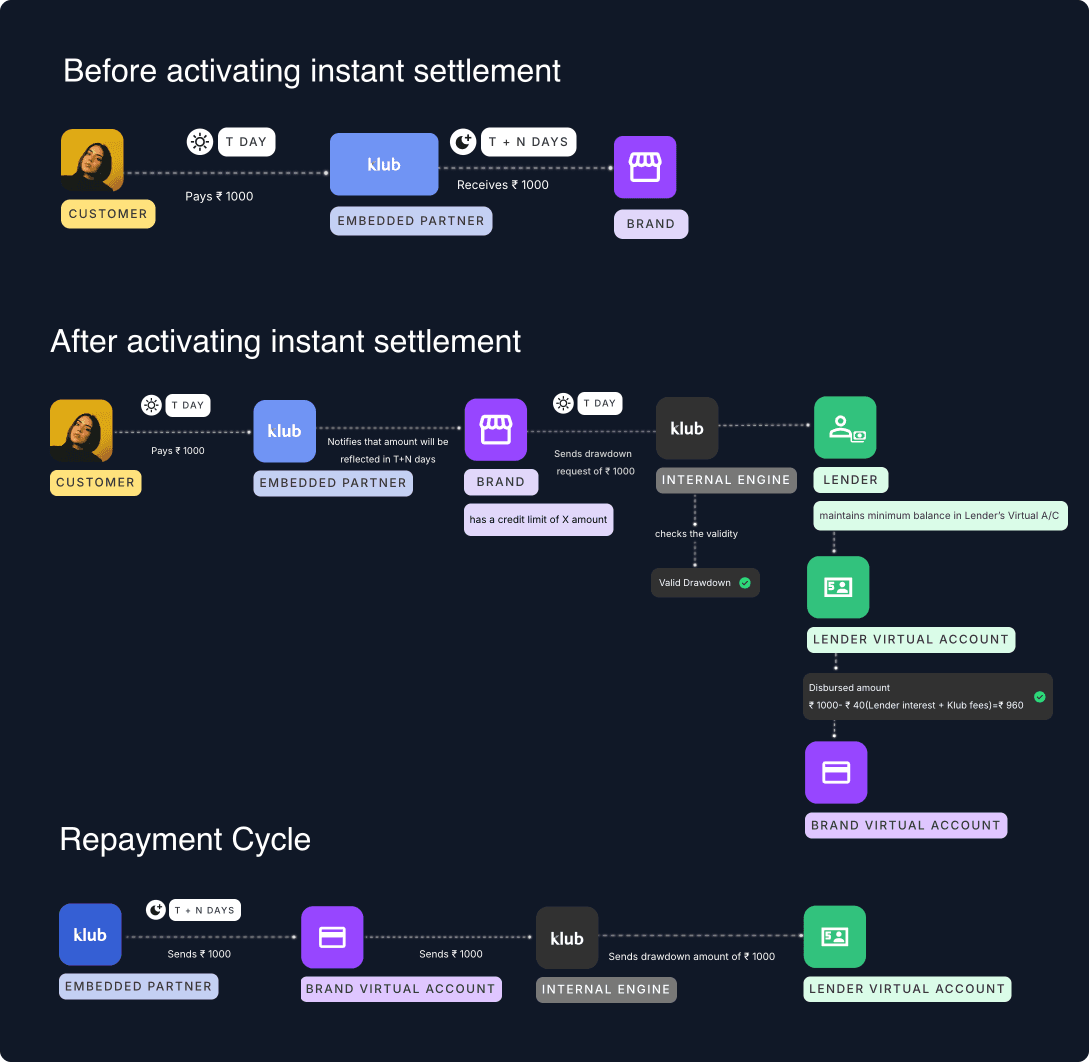

In eCommerce, getting paid can take a long time. Merchants sometimes have to wait days or weeks to get the money from what customers buy. This makes it hard to manage money and can be frustrating when they need to pay bills or buy more things to sell.

Instant Settlement is one of a kind fin-tech solution that provides immediate remittance of funds. Klub identified this opportunity to offer a product that ensures same day settlement, thereby enabling merchants to unlock growth opportunities, enhance customer satisfaction, and optimise their financial operations.

Klub's Benefits

Merchant Benefits

Lender Benefits

Simplifying the Complex

Klub has two platforms, Brands app and Capital Partner Platform. Shipping & e-commerce platforms tie up with Klub as Embedded Partners, and brands can directly apply for capital via the promotional banner shared at the embedded partner’s platform or Partner Marketplace.

In a team of two designers, I was responsible for the Lender’s or Capital Partners Platform. Firstly, we worked on simplifying the instant settlement journey.

Setting the direction

After finalizing the entire mechanism, the next challenge was how to give product value to the lenders. In Capital Partner Platform, most of the tasks were to be automated by the Klub’s engine. This also meant that heavy volume of data will be generated since multiple transactions at high frequency can occur for one credit line.

Understanding Lender Needs

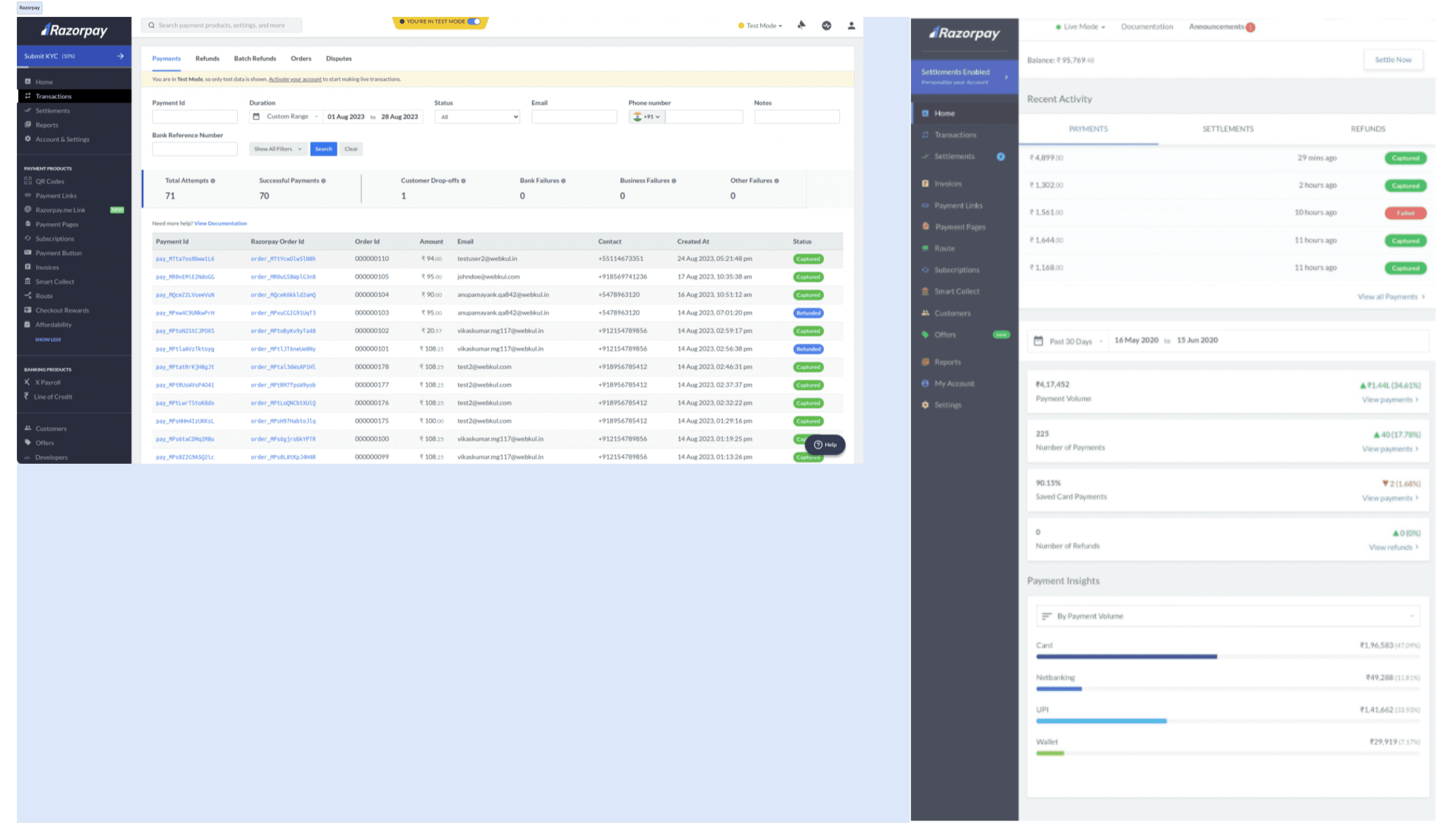

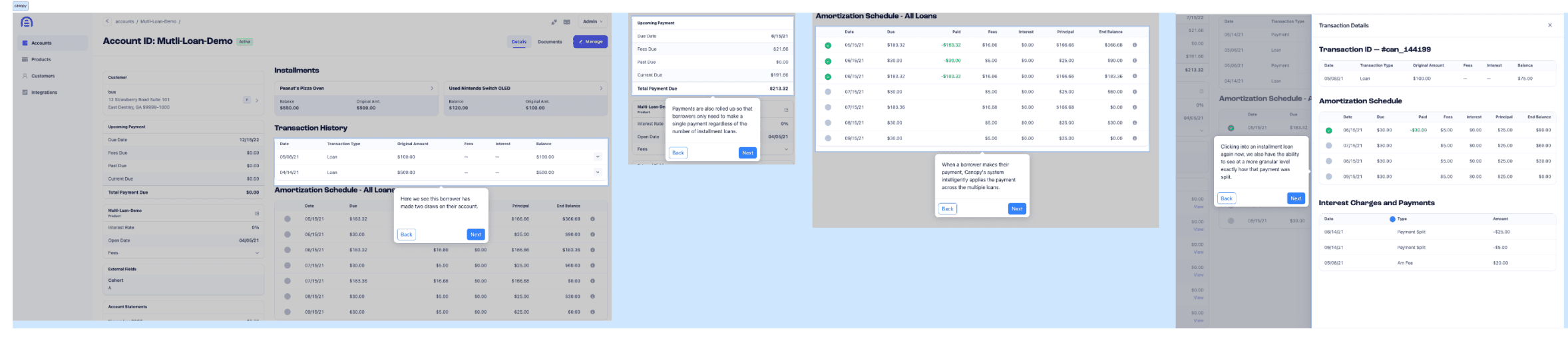

To understand how others have solved this problem, I did a competitive research. By analyzing the useflows, information hierarchy and interactions of competitors like Razorpay, PayU, Paytm and Mambu, I made a query list.

Solutions: Outstanding amount or available credit?

I worked with my cross-functional team of product and engineering to solve all these queries. Due to the complexity of the product, we decided to build some extra features which were not a part of the existing Capital Partner’s Platform.

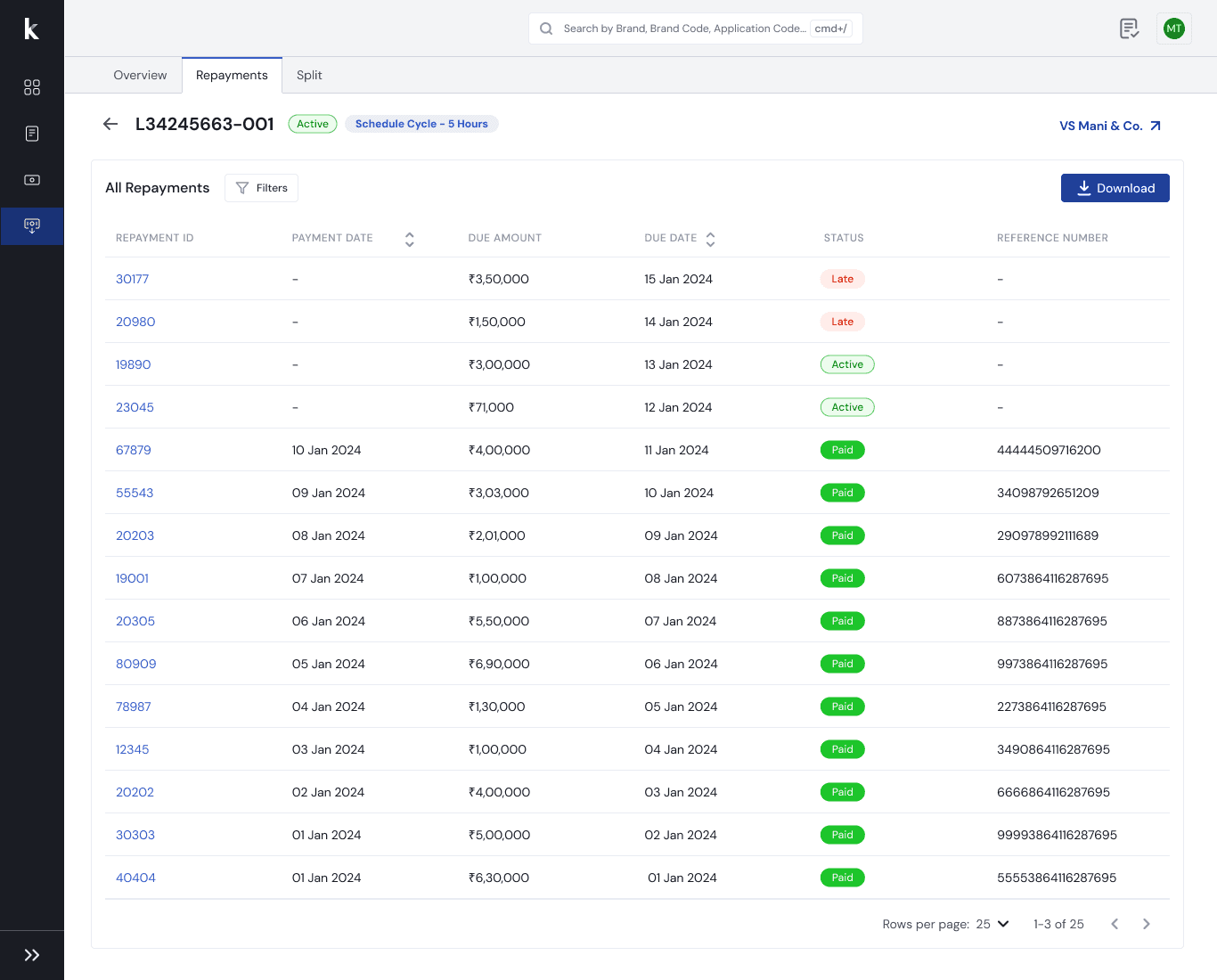

Solutions: Separate Section For Repayments

To avoid confusion, we decided to build a separate section for repayments.

Solutions: Linking a drawdown to a repayment?

The repayment ID will be clickable and open the list of all the drawdowns. This list of drawdowns will show drawdowns that are fully paid & partially paid (in-arrears). This entire list can be downloaded by the lender.

To conclude

Instant Settlement has been a major success for Klub, becoming a key revenue-generating product. It has significantly enhanced cash flow for merchants, strengthened partnerships, and contributed substantially to Klub's overall financial growth.